[Warning: this is a super-nerdy post that might trigger some people. If you don’t like…

Feeling Bullish? The 10 Best Uses For Your Tax Refund

It’s the end of the Australian financial year which means, for those who have incurred personal expenses in the course of their business, it’s tax return season and, ideally, tax refund season.

Much like the truffle season in Alba or the Indian wedding season for Gold prices, this can mean a flurry of expectant spending or, at the very least, plotting about what spending might ensue, assuming things work out favourably.

And irrespective of whether you have a tax refund in the offing, any time you have a lump sum coming your way, it’s a great opportunity to start building or growing your asset base.

So, in no particular order, here are some things to consider.

1. Clear Debts (Especially Credit Card)

You might think: so what?

A measly $1k on the credit card. No need to worry about that. Let’s buy some shares or a holiday or some fun (pick your poison, I don’t mind: wine, women, gear or gadgets. Even a fruity combination, perhaps).

NO. Not on your nelly, my friend.

The reason? Unless you have an interest-free card or have transferred a balance, you’ll be paying 15-25% on the credit card debt.

All your other investments will NOT be paying you anywhere near this much. At least on a consistent basis.

So earning at, say, 8% and borrowing (because that’s what your credit card really is) at 20% is a really, really bad idea. It’s also a bad idea that is compounded over time, so running a year-round CC balance in the 000’s is a fool’s paradise, my friend.

Big Time.

2. Pay Down Mortgage / Save For A Mortgage

Paying down your mortgage might not seem sexy.

In fact, there an entire industry geared around enticing you to do other things with you money. Ignore them, though, and seriously consider paying down your home loan.

But being mortgage-free, early, is a pretty cool thought.

If you don’t have own property yet, start thinking how you can accelerate the process.

This SFD article from GQ Australia How To Not Buy Property & Still Get Rich explains how you can fast-track saving for a deposit.

3. Invest In Yourself

How many new skills have your learned since you were 25?

For many of us it’s hard enough mastering the meagre skills we’ve been given or acquired so far.

But investing in ourselves and our future by cultivating our skill-set or talent stack is probably the most important investment we can make.

To a certain extent, it doesn’t even matter what you’re learning. Whether it’s learning a foreign language, taking a course on public speaking, learning to write code, the key thing is to be challenging and stimulating ourselves to develop and grow.

Do this and, almost by osmosis, your performance in all areas will soar.

4. Top Up Your Superannuation / Pension Fund

Propping up your pension with an after-tax lump sum isn’t as attractive as chucking in pre-tax and reaping the tax benefits offered by salary sacrificing, say.

And, it’s not really sexy.

BUT…

Don’t you want to have a comfortable retirement, especially given that there’s no telling how long we might live nowadays?

Also, once you’ve tucked it away in your pension, it’s there for a very long time, giving it a very love-you-long-time cogitation period. Which, in plain English, means it’s got plenty of time to grow and accumulate.

5. Become An Owner

Feeling emboldened now that you’re newly flush?

Hit the markets. Not the Farmer’s Markets, silly. The Stock Markets.

The problem is that unless you know what you’re doing, you’re likely to get rinsed.

Why?

Because there are plenty of professional trained and qualified finance-industry professionals who underperform their peers and the market in general.

What makes you think, you’re going to do any better than them? Arrogant, much?

A good way to get some exposure to the markets and become an owner (in a very tiny way, of course) of some of the world’s biggest and best companies is via managed funds.

Only the term “managed” here is something of a misnomer because the funds we’re interested in here are passively-managed funds which track the ‘index’ (that is, the stock market or index in a particular place).

Index funds are popular because they don’t carry the same kind of costs associated with actively managed funds. [Question: have you ever met a poor fund manager? No, me neither. It’s because your fees are paying for the Jag, the Rolex and their kid’s school fees.]

Not only are index funds cheaper than managed funds – often by 1-2.5% per year – they routinely outperform the funds with managers. Strange, huh?

The snappily-titled SPIVA (Standard & Poors’ Index Versus Active Funds) Scorecard demonstrated the following in Australia:

Over 5 years:

- 90% of active International Share managers underperformed against their index.

- 71% of active Australian Share managers underperformed against their index.

- 86% of Australian Bond funds underperformed.

- 81% of Property funds failed to beat the index.

For a more detailed analysis of this be sure to read this article.

Justin Brand also provides further supporting evidence about the performance of index funds versus managed funds in this article, which demonstrates that even hedge funds – the biggest, baddest and most exclusive of funds – struggle to outperform index-linked funds.

If any further evidence were need to advance the argument in favour of index funds, check this out.

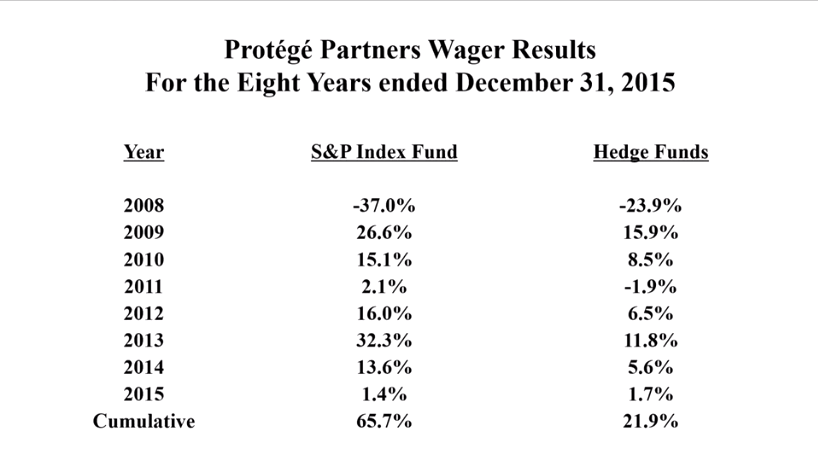

These are the results to date from a $1m bet Warren Buffett – the world’s greatest investor – made against Protege Partners, a hedge fund with $3.5bn under management. It was a 10 year bet and, whilst it’s not yet over, the lead is almost unassailable.

He’s smashing them.

Read more about the bet here.

So if you’re looking for a proven way to create and grow wealth over a long time-frame (10+ years), the stock markets and index-linked funds tread a proven path.

Or you could…

6. Buy Individual Stocks

Not for the faint-hearted, this can be an exciting ride.

If you get a tip from a mate about a firm that makes mining valves and supplies a firm who’ve just found a massive unknown copper deposit somewhere in the middle of Whup-Whup, well, you could be quids in.

I wasn’t. And African Diamonds was another red-hot smoker. And Stratex. But, somewhat surprisingly, more prosaic holdings in HSBC and Vodafone performed better. So did Easyjet.

The point is this: you’re unlikely to get any information before hundreds and thousands of others have that same information. That hot tip your mate gave you has been through brokers and dealers and market-makers. People will be all over it.

If it’s truly fresh information, it’s probably illegal. In which case, fill your boots, but don’t leave a trail.

All, cough-cough, jokes aside, if you do buy individual shares you might want to look at solid blue chip shares with a history if delivering strong earnings growth and Return On Equity (ROE).

You might be attracted to a decent 4+% dividend, reasoning, not unreasonably, that a 4% return on top of any growth in the share price is a fairly handsome return.

The golden rule, though: always tick the box to have your dividends invested. Never deviate from this and you should be okay [assuming your stock pays a dividend].

7. Give It Away

Percentage of people ticking this option: a big fat zero [I’d love to be proved wrong here, by the way].

But imagine how good it would make you feel.

To help those less fortunate in a meaningful way. How absolutely magnificent.

GIVE WELL ranks charities according to how effective they are with their donations. This means you can give to charities that have the least waste and give the most to the intended beneficiaries.

At the very least consider making a monthly donation via direct debit to one of the Give Well top-rankers.

8. Travel

They say nothing broadens the mind like travel.

Which is tricky because if you’re a new-ish parent, the idea of transporting your chaotic sleep-deprived existence to somewhere unfamiliar where you don’t know the name of the barista or the nearest 24 hour petrol station for the late-night banana dash.

But whether you’re encumbered by kids or not, it’s never that bad.

It’s actually wonderful. The whole family seem to recognise the importance of the trip and improve their behaviour tenfold.

Even the dog.

9. Buy Art

If none of the options listed before appeal, and coke and hookers are off limits, then there are a couple of other options to consider.

I select them over the aforementioned bugle and strumpets because they have the potential to be appreciating assets.

If you can cultivate an appreciation of art, I think it can be useful. Finding something (as in, a piece of art) that resonates with you and can calm you when seas get stormy can be a real comfort.

Go for what appeals to you, not what you think you should like.

Once you see it, you’ll know.

10. Buy Jewellery

This is basically: a watch.

A watch says an awful lot about a chap.

A walked into my boss’ office once and found him preening about, one shirt sleeve pulled up with what looked to be a wall clock on his wrist.

“New watch,” I said.

“Yep,” he said.

“What brand,” I said, squinting to try and see the dial.

“Guess,” he said.

“Breitling,” I said, knowing he’d recently been given more responsibility and, therefore, more dough.

Turns out it was actually a Guess watch.

Each to their own, I suppose.

I realise we could easily disappear down a wanky rabbit-hole here so I’ll impart what I know. Or, rather, what I’ve been told by a watch and diamond dealing chum.

If you want a watch that will possibly appreciate in value, solid brands are: Rolex, Cartier, Panerai. If you can afford a Patek Philippe then you probably don’t need my advice.

Audemars Piguet come in for repairs a lot. Panerai don’t tell the time very well.

Rolexes give their owners the least trouble.

Conclusion

As we’ve seen there are a myriad of options and we’re in danger of suffering from a Paradox Of Choice when it comes to using our tax refund wisely.

There are other things I couldda and shouldda mentioned – robo-advice being something that can be closely aligned with index funds (and something I’ll touch on soon), and seed or angel investing for those with an established portfolio or a cavalier approach to risk.

The best wine is enjoying amazing price rises at the moment, too.

But, in the interests of expedience, we’ll leave it there for now.

At the very least, buy something that will appreciate and grow or will help you or someone else appreciate and grow. As long as you do that, you’ll be winning.

[optin_box style=”15″ alignment=”center” email_field=”email” email_default=”Enter your email address” integration_type=”mailchimp” double_optin=”Y” thank_you_page=”https://superfitdad.com.au/thank-you/” list=”ea125ae213″ name_field=”FNAME” name_default=”Enter your first name” name_required=”Y” opm_packages=””][optin_box_field name=”headline”]Get More Finance Hacks[/optin_box_field][optin_box_field name=”paragraph”]PHA+R3JhYiBteSBsaWZlIGhhY2tpbmcgZWJvb2ssIGphbW1lZCB3aXRoIGZpbmFuY2UgYW5kIGZpdG5lc3MgdGlwcyB0byBnZXQgeW91IGhlYWx0aHksIHdlYWx0aHkgJmFtcDsgd2lzZS48L3A+Cg==[/optin_box_field][optin_box_field name=”privacy”]We Love You Too Much to Spam You![/optin_box_field][optin_box_field name=”top_color”]undefined[/optin_box_field][optin_box_button type=”1″ text=”Yes Please” text_size=”32″ text_color=”#000000″ text_bold=”Y” text_letter_spacing=”0″ text_shadow_panel=”Y” text_shadow_vertical=”1″ text_shadow_horizontal=”0″ text_shadow_color=”#f8f8f7″ text_shadow_blur=”0″ styling_width=”40″ styling_height=”30″ styling_border_color=”#000000″ styling_border_size=”1″ styling_border_radius=”6″ styling_border_opacity=”100″ styling_shine=”Y” styling_gradient_start_color=”#f1f505″ styling_gradient_end_color=”#ffffff” drop_shadow_panel=”Y” drop_shadow_vertical=”1″ drop_shadow_horizontal=”0″ drop_shadow_blur=”1″ drop_shadow_spread=”0″ drop_shadow_color=”#000000″ drop_shadow_opacity=”50″ inset_shadow_panel=”Y” inset_shadow_vertical=”0″ inset_shadow_horizontal=”0″ inset_shadow_blur=”0″ inset_shadow_spread=”1″ inset_shadow_color=”#ffff00″ inset_shadow_opacity=”50″ location=”optin_box_style_15″]Yes Please[/optin_box_button] [/optin_box]

Related Posts